.png?width=165&height=66&name=Untitled%20design%20(9).png "Untitled design (9)")

Three changes in one announcement, and a math problem most coverage is skipping.

The 50 percent CGT discount is gone. That's the headline. It's also the wrong place to stop reading.

The Budget 2026 CGT reform isn't one change. It's three. And whether you end up paying more or less under the new rules depends on something most coverage hasn't bothered to model: your real rate of return.

This edition resolves what the reform actually is, how the transitional split at 1 July 2027 works in practice, and why two investors holding identical properties can land on opposite sides of the new math. It matters because the decision to hold, sell, or restructure ahead of 2027 hinges on numbers the headlines have skipped over.

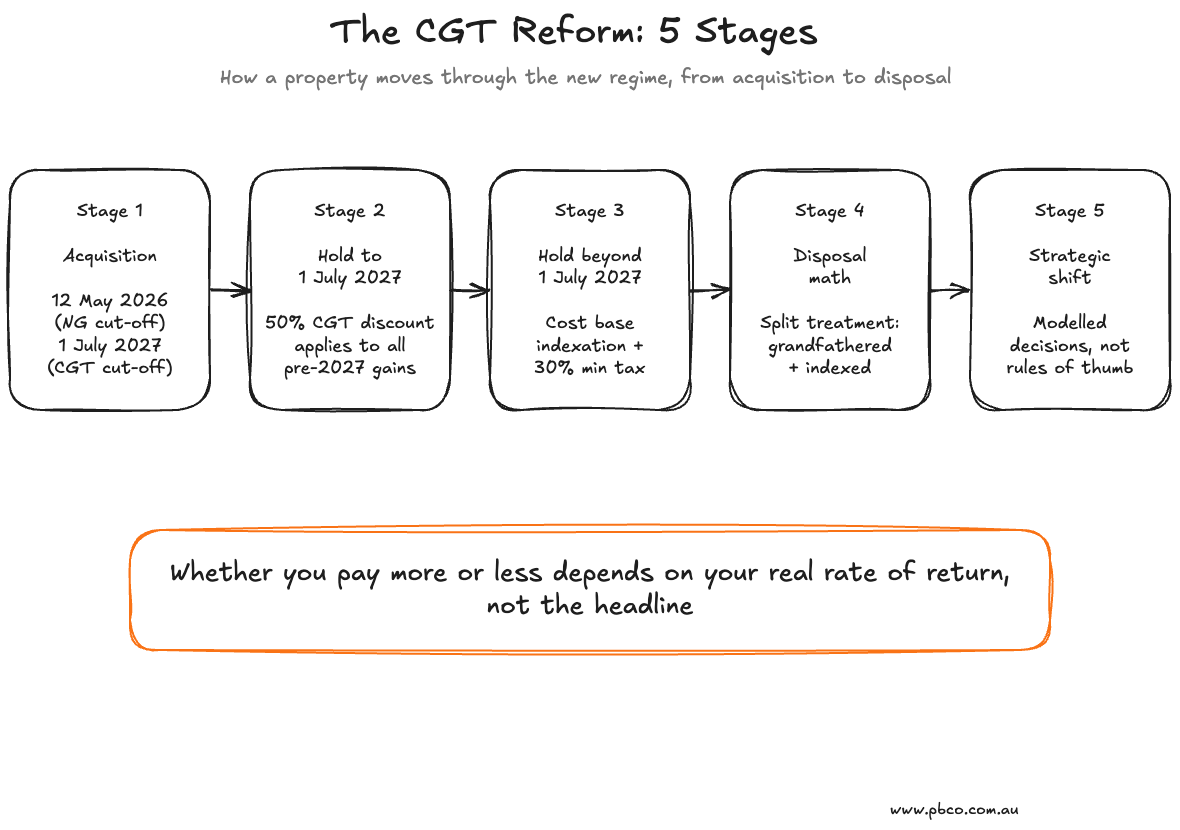

Stage 1: Acquisition

The acquisition date matters in two different ways.

- For negative gearing, properties acquired before 7:30pm AEST on 12 May 2026 are grandfathered. After that date, only new builds keep the negative gearing concession.

- For CGT, the timing of acquisition mostly doesn't matter. The split is at 1 July 2027, not 12 May 2026. Even pre-1985 assets (which were exempt when CGT was first introduced) are caught for gains accruing from 1 July 2027.

Key insight: The negative gearing change has a 12 May 2026 cut-off. The CGT change has a 1 July 2027 cut-off. They aren't the same date and they aren't the same scope. Most people are conflating the two.

Stage 2: Hold to 1 July 2027

Every CGT asset gets a valuation point on 1 July 2027. At sale, the taxpayer determines the asset's value at that date in one of two ways:

- A formal valuation as at 1 July 2027

- The ATO-provided apportionment formula, which estimates value based on the asset's growth rate over the hold

The 50 percent CGT discount applies to all gains accrued before this date. That portion of the gain is locked in under the old rules. It does not change, regardless of what happens after.

Key insight: Existing investors keep the 50 percent discount on everything earned to 1 July 2027. The longer the hold from purchase to that date, the more of the lifetime gain stays grandfathered.

Stage 3: Hold Beyond 1 July 2027

From 1 July 2027 onwards, two things change for individuals, trusts, and partnerships. Super funds (including SMSFs) and widely held trusts are excluded.

- Cost base indexation. The cost base from 1 July 2027 is increased each year by CPI, reducing the nominal gain to a real gain at sale.

- 30 percent minimum tax on real gains. Investors whose marginal rate in the disposal year would otherwise sit below 30 percent get topped up to 30 percent. Those already paying 30 percent or more aren't affected by this part.

Indexation is friendly to slow-growing or inflation-tracking assets. The 30 percent minimum is targeted at investors who time disposals to low-income years (think retirees realising in a year with no salary). Together they replace the simpler 50 percent discount with something more conditional.

Key insight: Indexation rewards low real returns and punishes high ones. The math depends on the specific asset, not the headline.

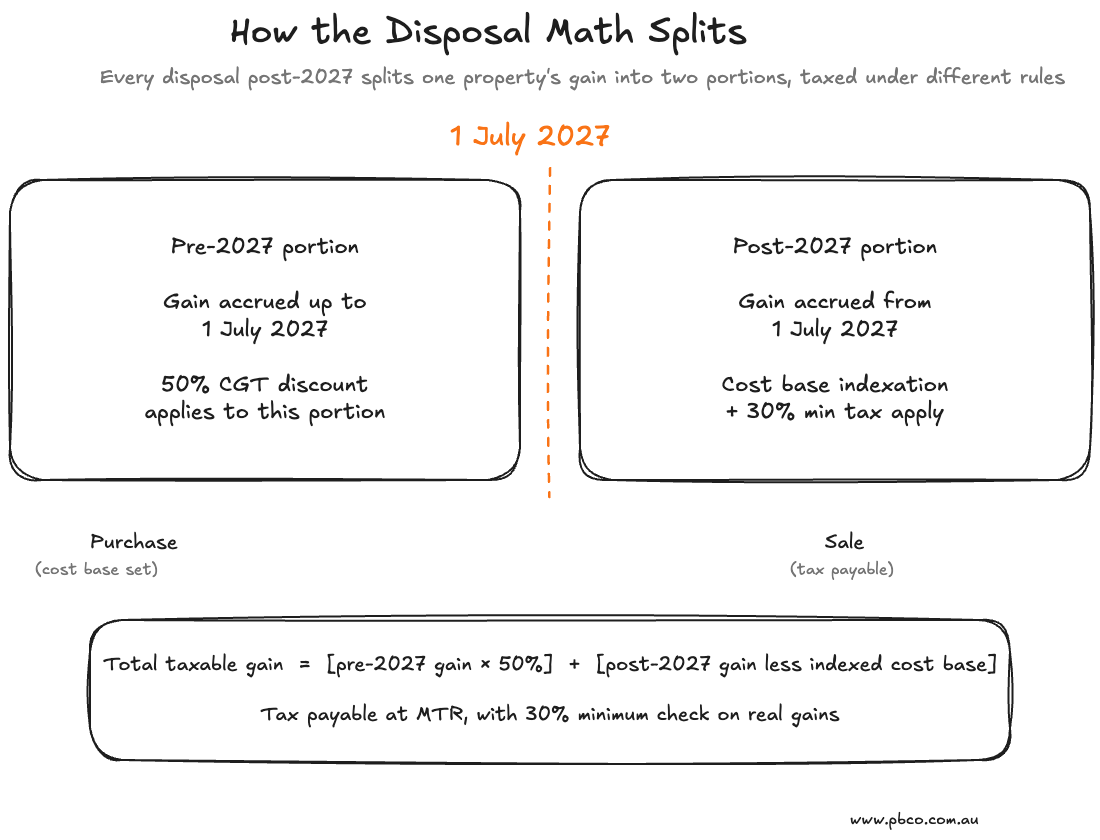

Stage 4: The Disposal Math

At disposal post-2027, the gain is split into two portions and taxed differently.

- Pre-2027 portion: (value at 1 July 2027 minus cost base) × 50 percent discount = taxable

- Post-2027 portion: sale price minus indexed cost base at 1 July 2027 = taxable

- Total taxable gain is the sum of the two

- Tax payable is total taxable gain at marginal rate, with the 30 percent minimum applied to the real gain

The punchline most coverage skips: whether you pay more or less under the new regime depends almost entirely on your real (after-inflation) rate of return on the post-2027 portion.

- Real return at or below inflation: you pay less than under the old discount

- Modest real return around 2 to 3 percent pa: outcomes are roughly the same

- Strong real return of 4 percent pa or above: you pay more, sometimes materially more

Key insight: The reform isn't a flat tax hike on property. It's a redistribution. It taxes inflation-tracking assets less and strong-growth assets more.

Stage 5: The Strategic Shift

Three things change about how a serious investor thinks under the new regime.

- Rules of thumb stop working. The right answer for hold and sell decisions now depends on your specific cost base, your 1 July 2027 valuation, and your assumed growth rate. You can't apply a flat 50 percent discount in your head anymore. Every disposal decision becomes a modelled decision.

- The negative gearing carve-out isn't a clean asset-allocation play. Negative gearing is restricted only on residential property. Shares and commercial property keep their negative gearing arrangements unchanged. KPMG noted this "may well impact investment allocation decision making" specifically for negative gearing. But the CGT change is broader. It catches all CGT assets held by individuals, trusts, and partnerships, shares included. The advantage isn't "non-residential is now better" across the board. It's "non-residential keeps the negative gearing benefit, while CGT becomes neutral across asset classes." Two different lines, often conflated.

- Strong-growth markets need a recalibrated hold strategy. The longer you hold a high-growth asset past 1 July 2027, the larger the cumulative excess tax versus the old regime. The crossover between paying more and paying less sits roughly at the long-run residential growth rate.

Key insight: KPMG calls this "a paradigm shift in our capital gains tax rules." That's not political colour. It's a senior tax partner's plain reading. The investors who get this right will be the ones who model the decision properly. The ones who don't will find out at disposal.

Sam's Case Study

Sam is 41. He owns one investment property, a 3-bedroom western corridor house bought 18 months ago for $710,000. The property is grandfathered for negative gearing under the 12 May 2026 announcement.

He runs the math on a 10-year hold from policy commencement to understand his exposure under the new CGT regime.

At 1 July 2027, the property has been held for around two and a half years. Under a 5.5 percent pa nominal growth assumption, its value at that date would be around $822,000. He models three scenarios from there.

| 10-yr growth | Sale value (~2037) | Tax under new regime | Tax under old regime | Net change |

|---|---|---|---|---|

| 3 percent pa | $1,043,000 | $32,000 | $62,000 | $30,000 better |

| 5.5 percent pa | $1,404,000 | $151,000 | $128,000 | $23,000 worse |

| 7 percent pa | $1,711,000 | $254,000 | $185,000 | $69,000 worse |

Figures assume 2.5 percent inflation, 37 percent marginal tax rate, full 50 percent discount under the old regime, indexation plus 30 percent minimum tax check under the new.

The numbers tell Sam three things.

His property doesn't have one tax outcome under the new regime. It has a range, indexed to growth. The crossover where he becomes worse off is around 4 to 5 percent pa nominal growth, close to the long-run residential average. A high-growth scenario costs him close to 40 percent more tax than the old regime. A low-growth scenario saves him about half.

Sam decides to model the same property at shorter hold horizons (5 and 7 years) and revisit annually. He doesn't sell pre-2027. He treats the 1 July 2027 valuation as a critical data point to lock in, not avoid.

Reflection

The Budget 2026 CGT reform has been read as a tax hike on property investors. It's something narrower and stranger than that. It's a structural change that hits some assets and rewards others, decided by a math problem the headlines aren't running. The investors who get this right will be the ones who model the decision properly. The ones who keep running rules of thumb will be wrong-footed at disposal, and won't realise it until the tax bill arrives. As Sun Tzu put it, "He will win who knows when to fight and when not to fight." Same logic applies to selling. The new regime makes that decision harder. It also makes getting it right more valuable.

See you next week. — Alex

If this was useful, share it with someone trying to figure out the same thing. And if you're not subscribed yet, you can join the list at pbco.com.au.

Next week: The Sequence Problem.

This article is for educational purposes only. It does not constitute financial, legal, or tax advice. Everyone's circumstances are different. Please seek professional advice before acting on any of the strategies outlined above.